![]() LIMOGES, France — Legrand today announced its results for the first nine months of 2024.

LIMOGES, France — Legrand today announced its results for the first nine months of 2024.

Benoît Coquart, Legrand’s Chief Executive Officer, commented:

For the first nine months of the year, sales (excluding currency effects and our exit from Russia) were stable, in a building market that remains in decline in most of our geographies. In the third quarter alone, sales growth (+2.4% excluding currency effects and Russia) was driven in particular by sustained growth in datacenters in the United States.

Our financial indicators remain solid, in terms of both margins and free cash flow.

Our external growth has been very dynamic this year, with 7 acquisitions announced, including 4 in the buoyant datacenter sector, demonstrating Legrand’s ongoing ability to strengthen its leadership positions through value-creating operations.

Fully confident in our strategy, we are specifying our annual targets as communicated at the beginning of February, and are resolutely pursuing the implementation of our 2030 roadmap, as presented at our Capital Markets Day on September 24. This roadmap is supported in particular by the buoyant field of energy and digital transition, which already represented 46% of sales in 2023.

2024 full-year targets specified

In 2024, the Group is pursuing the profitable and responsible development laid out in its strategic roadmap.

Taking into account the achievements on the first nine months of the year as well as the world’s current macroeconomic outlook, and with confidence in its model for creating integrated value, Legrand has specified its full-year targets for 2024:

- low single-digit sales growth (organic and through acquisitions – unchanged);

- an adjusted operating margin after acquisitions of between 20.0% and 20.4% (vs. between 20.0% and 20.8% before acquisitions previously);

- at least 100% CSR achievement rate for the third year of the 2022-2024 roadmap (unchanged).

Financial performance as of September 30, 2024

Consolidated sales

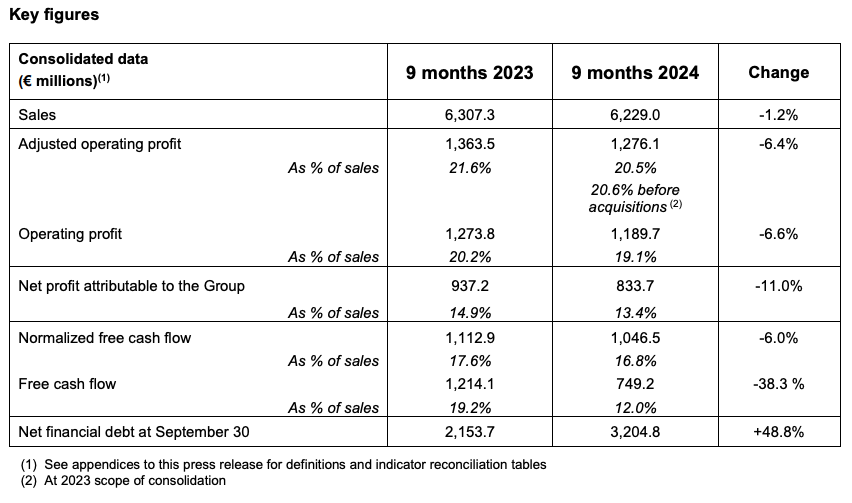

In the first nine months of 2024, sales were down a total of -1.2% from the same period of 2023, at €6,229.0 million [USD 6,727.32 million].

In a building market which remains depressed in many geographies, the organic decline in sales was -0.8% over the period, including -0.1% in mature countries and -2.8% in new economies.

The impact of a broader scope of consolidation was +0.3%, including +1.1% linked to acquisitions and -0.8% due to the impact of the Group’s disengagement from Russia. Based on acquisitions made and their likely dates of consolidation, their overall impact should be close to +2% full year, of which nearly +2.5% linked to acquisitions and -0.6% to the impact of disengagement from Russia as of October 4, 2023.

The exchange-rate effect on sales in the first nine months of 2024 was -0.7%. Based on average exchange rates in October 2024 alone, the full-year effect should be around -1% in 2024.

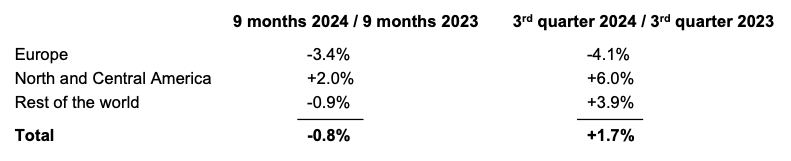

Changes in sales by destination at constant scope of consolidation and exchange rates broke down as follows by region:

These changes are analyzed below by geographical region:

- Europe (40.1% of Group revenue): in a building market that remains difficult in most countries, sales at constant scope of consolidation and exchange rates fell by -3.4% over the first nine months of 2024, and by -4.1% over the third quarter alone. These trends reflect a particularly deteriorated context in mature countries during the quarter, and do not point to a recovery in the construction market in the very short term.

- Sales in Europe’s mature economies (35.0% of Group sales) fell organically by -3.7% over the first nine months of 2024, of which -5.3% in the third quarter alone. Italy and the UK held up well over the first nine months, but failed to offset a decline in sales in France, Spain, Germany and the Netherlands in particular.

- Sales in Europe’s new economies were down -1.3% over the first nine months of the year. In the third quarter alone, sales rose by a healthy +4.7%, with a growth in Eastern European sales.

- North and Central America (40.1% of Group revenue): sales were up +2.0% from the first nine months of 2023 at constant scope of consolidation and exchange rates.

- In the United States alone (36.8% of Group revenue), sales rose +3.1% in the first nine months of the year, including a steep +7.2% rise in the third quarter alone. The 9-month performance was mostly driven by offers dedicated to the datacenter segment.

- Over the first nine months, sales declined in Canada and Mexico.

- Rest of the world (19.8% of Group revenue): sales marked an organic decline of -0.9% in the first nine months of 2024.

- In Asia-Pacific (12.2% of Group revenue), sales declined by -3.8% over the 9-month period and by -3.2% in the third quarter alone. Over the first nine months, growth in India was unable to offset the sharp fall in China, where the construction market continues experiencing a marked decrease.

- In Africa and the Middle East (3.6% of Group revenue), sales were up +4.4% in the first nine months of the year and +25.7% in the third quarter alone. Over nine months, sales trends were sustained in the Middle East and showed a slight decline in Africa, which saw a strong recovery in the third quarter alone.

- In South America (4.0% of Group revenue), sales were up +3.8 % in the nine first months, with marked growth in Brazil, and advanced a strong +7.6% in the third quarter alone.

Adjusted operating profit and margin

Adjusted operating profit for the first nine months of 2024 stood at €1,276.1 million [USD 1,378.19 million], down -6.4% from the first nine months of 2023. This corresponds to an adjusted operating margin equal to 20.5% of sales for the period.

Before acquisitions, adjusted operating margin for the first nine months of 2024 stood at 20.6% of sales, down -1.0 point from the first nine months of 2023.

Over this period, Group profitability confirmed Legrand’s ability to maintain high margins despite a decrease in sales.

Value creation and solid balance sheet

Net profit attributable to the Group came to €833.7 million [USD 900.40 million], down -11.0% from the first nine months of 2023 and equal to 13.4% of sales. This trend was due primarily to a decline in operating profit, the negative impact of financial results and exchange-rate effects, and a corporate income tax rate of 27.0% for the first nine months of 2024.

Free cash flow came to 12.0% of sales over the period, to total €749.2 million [USD 809.14 million].

The ratio of net debt to EBITDA stood at 1.7 on September 30, 2024, a level that reflects the pace of acquisitions since the beginning of the year as well as a solid free cash flow generation.

In addition, as previously announced, Legrand will have to pay an amount of €43 million [USD 46.44 million] following the decision by the French Competition Authority regarding the application of derogated prices on the French market between 2012 and 2015. Legrand categorically rejects the allegation made against it and reserves the right to appeal this decision.

Strong acquisition momentum

This year, Legrand pursued external acquisitions at a robust pace. The 7 operations announced in 2024 represent acquired annual sales of almost €350 million [USD 378 million] and include:

- in the buoyant datacenters segment, the acquisition of Netrack (Indian specialist in racks), Davenham (Irish specialist in low-voltage power distribution systems), Vass (Australian leader in busbars) and UPSistemas (Colombian specialist in the integration, commissioning, maintenance and monitoring of technical infrastructures);

- in the assisted living and connected health segment: Enovation, the Dutch leader in connected health software;

- lastly, in the essential infrastructures segment: MSS in New Zealand and APP in Australia.

Legrand intends to continue strengthening its leadership positions with value-creating acquisitions.

2030 ambitions and growth pillars

Legrand hosted a Capital Markets Day in London on September 24, 2024.

This event was an opportunity for the Group to present its strategy both for essential infrastructures products (54% of its 2023 revenue) and for solutions that support the energy and digital transition (46% of its 2023 revenue, including products for datacenters, energy transition, and digital lifestyles).

Legrand detailed its 2030 ambitions, with:

- Sales in 2030 in a range of €12 to 15 billion [USD 12.96 to 16.20 billion], including sales growth excluding the impact of exchange rates of between +6% to +10% in CAGR. This includes +3% to +5% organic CAGR and +3% to +5% CAGR related to acquisitions,

- Average adjusted operating margin of around 20% of revenue, including +30 to +50 basis points of annual organic improvement and -30 to -50 basis points of annual dilution from acquisitions,

- Free cash flow generation of nearly €10 billion [USD 10.80 billion] from 2025 to 2030, with average free cash flow ranging between 13% and 15% of sales, an average Capex to sales ratio of 3% to 3.5%, and an average working capital requirement ratio of 10% of sales or less,

- A capital allocation policy prioritizing acquisitions (at least 50% of average free cash flow) and an attractive dividend payment (with a distribution ratio of around 50%). Over the period, a total of around €5 billion [USD 5.40 billion] will thus be dedicated to acquiring companies to round out the Group’s products and geographical range,

- 80% of total sales qualifying as eco-responsible sales, and reducing Scope 1, 2 and 3 emissions in line with Legrand’s Net Zero 2050 commitment.