TrendForce’s lighting market research indicates a noticeable improvement in inventory depletion for lighting companies compared to the first half of 2023. Growth has been seen in outdoor lighting orders and renovation projects. However, demand remains subdued across most retail, indoor lighting, and specialized lighting sectors. The gloomy global economy this year has also led to a consolidation phase in the lighting market, resulting in stable overall demand. Consequently, TrendForce anticipates a slight YoY decrease of about 5% in the revenues of the world’s top ten lighting manufacturers for 2023. Despite the ongoing uncertainty in the lighting market, after two years of adjustment, a resurgence in demand is anticipated in the second quarter of 2024.

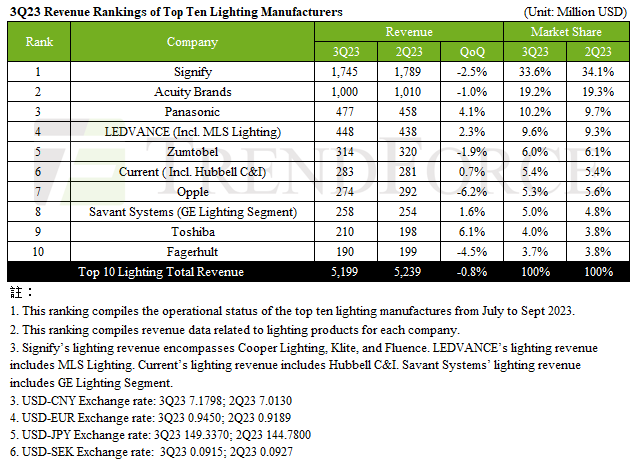

The third quarter performance of various companies suggests slight revenue recovery. The top ten lighting companies’ combined revenues reached US$5.2 billion, a slight QoQ increase of 0.8%. Signify, Acuity Brands, and Panasonic lead the top three, collectively accounting for about 63% of the total revenue. Except for the swap in rankings between LEDVANCE and MLS Lighting with Panasonic, the rest maintained their positions from previous quarters.

Signify’s third-quarter revenue was approximately US$1.75 billion, a 2.5% decrease from the previous quarter. This decline in revenue is primarily attributed to continuous weak demand in retail and indoor lighting, as well as a slowdown in OEM sales. The company saw significant revenue dips in key European markets, such as Germany, Belgium, the Netherlands, Luxembourg, and the UK, and also in North American markets, including the U.S. and Canada. Recovery in the Chinese market also fell short of expectations.

Acuity Brands reported close to US$1 billion in revenue for the third quarter, down 1% from the previous quarter. This decline in lighting revenue was linked to extended product replacement cycles and the overall economic downturn. Still, the company maintains its position in the global top three, representing roughly 20% of total revenue among the top ten lighting manufacturers. In 2023’s first half, Acuity Brands launched its innovative Design Select project to offer customers high-quality lighting products and solutions. This initiative includes around 3,000 selectable products from leading brands such as Aculux, Gotham, Lithonia, nLight, and SensorSwitch.

Overseas operations now contribute over 50% to MLS Lighting’s overall revenue following its acquisition of LEDVANCE. For the first three quarters of 2023, lighting sales constituted 73% of total revenue, with the latter half primarily bolstered by seasonal demand in China’s lighting industry. However, a saturated overseas market has restrained growth, reflected in MLS Lighting’s third-quarter performance, which saw a modest increase of about 2.3%. Notably, LEDVANCE performed well in China’s industrial lighting market in the first half of 2023. With strategic positioning and product upgrades, LEDVANCE’s annual lighting revenue is expected to grow throughout the year.

For more information on reports and market data from TrendForce’s Department of Optoelectronics Research, please click here, or email the Sales Department at OR_MI@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://www.trendforce.com/news/

Tagged with lightED, lighting