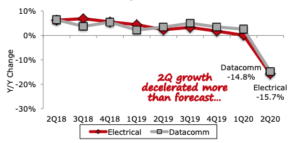

The exclusive tED magazine/Robert W. Baird research on the second quarter of 2020 for electrical distributors shows a difficult April and May followed by some recovery in June. Analysis from Baird shows continuing recovery in the third quarter of this year, but still well below revenue levels when compared to the third quarter of 2019.

The exclusive tED magazine/Robert W. Baird research on the second quarter of 2020 for electrical distributors shows a difficult April and May followed by some recovery in June. Analysis from Baird shows continuing recovery in the third quarter of this year, but still well below revenue levels when compared to the third quarter of 2019.

The research shows the second quarter was work than forecast, with revenue down early 16% in electrical and nearly 15% in Datacomm. Back in April, tED magazine reported the first quarter of 2020 results, which included a prediction of an 11.8% drop in revenue in electrical and 11.5% in Datacomm for the second quarter. The declines for NAED members is nearly double the 9.8% decline in revenue seen across the broader distribution industry.

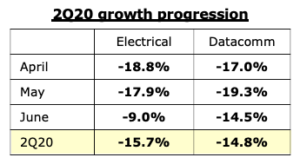

Breaking down the second quarter month-by-month, NAED distributors saw their largest revenue decreases in electrical and Datacomm during April, when revenue was down 18.8% and 17% when compared to April of 2019. Revenue was also difficult in May, as electrical saw a 17.9 decrease in revenue while Datacomm’s loss was 19.3%. The rebound came as economies started to reopen in June, with electrical revenue’s dip at 9% and Datacomm posting a 14.8% decrease in revenue.

Comments from the NAED respondents to the survey reflected the difficult quarter, but also some optimism for the rest of the year.

- “May seemed to be the bottom. June got stronger as the month trended on. Daily order rates up about 10% in June over May. Hope it continues to gain throughout 3Q”

- “Cautiously optimistic on the rebound, but we are seeing bumps in the road already.”

- “Revenue from non-residential market is rebounding. Non-residential is still slow.”

- “On our industrial OEM side, I believe that they ran down inventory in April and May and are now only filing new orders, but no yet increasing inventory.”

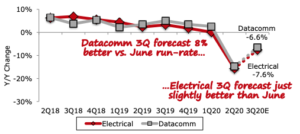

For the third quarter of 2020, responded expect to see a continued improvement, but still will not reach 2019 numbers for revenue. Distributors expect revenue for electrical to be down 7.6% over the next three months, and Datacomm down 6.6%.

One key result of the downturn: pricing. While the average pricing is down less than 1% for the second quarter, the real issue will be competition, where distributors are competing for fewer dollars.

- “Getting more aggressive in quoting projects or spot buys, but not really showing up in the numbers.”

- “Increased pricing pressures as competition looks to win business to get any revenue in the door.”

- “Smaller pie with many people looking to have a piece.”

- “I see price increases coming from vendors and it is likely due to credit risk. We will be looking at passing inflationary and credit risk costs of doing business to our customers.”

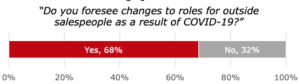

As far as the long-term impact of the COVID-19 crisis, NAED members are looking at a number of strategy changes in the next 12 months. 89% of the respondents say they will make either minor or major changes to strategy in the next year. One of those changes could come in the responsibilities of outside salespeople. More than two-thirds of the responses say they foresee changes in role for outside salespeople.

Potential changes include:

- “Much more virtual contact and less personal face to face opportunity.”

- “More time on social media following up and less time driving.”

- “Look to leverage technology at a far greater rate.”

- “Outside sales will become more solution-focused and will have a split of somewhere around 70% inside and 30% outside.”

- “Outside sales has been marginalized by the customer. Customers are being accelerated into digital transformation seeking omni channel solutions.”

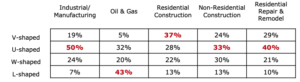

When it comes to recovery, respondents to the tED magazine/Baird study broke down the different segments and potential shapes for recovery. Industrial/Manufacturing, Non-Residential Construction, and Residential Repair and Remodel are expected to take on a U-shaped recovery, while Residential Construction is expected to have a V-shaped recovery and Oil & Gas is expected to take on an L-shaped recovery.

Responses ranged from hopeful to a near “knock-out”.

- “My sales team is reporting industrial will still be very soft for another 2-3 months, and even then won’t get back to 2019 levels.”

- “Industrial new construction significantly off, leading to lower revenue.”

- “One-two punch: Oil and gas collapsed followed by COVID-19. Almost a knock-out.”

- “Just about all business activity is servicing projects booked 6+ months ago. There are very few large projects that we expect to bid on over the next 2 months.”