HARVEY, Ill. — Atkore Inc. announced earnings for its fiscal 2023 second quarter ended March 31, 2023.

HARVEY, Ill. — Atkore Inc. announced earnings for its fiscal 2023 second quarter ended March 31, 2023.

“Atkore delivered solid results in the second quarter, highlighted by a significant increase in cash flow from operating activities versus the prior year,” said Bill Waltz, Atkore President and Chief Executive Officer. ”Our mid single-digit volume growth, which is in line with our full year expectations, reflects the resilience of our business model, diversification of our portfolio and efforts of our team. Strong performance of our solar related products contributed to the 20% volume growth of our Safety and Infrastructure segment. With the performance we’ve achieved in the first half of the year and the positive trends we are experiencing, we are increasing and narrowing our outlook for Adjusted EBITDA and Adjusted EPS for Fiscal Year 2023.”

Waltz continued, “We continue to execute our capital deployment model by investing in our business and returning capital to shareholders. We repurchased $119 million in stock during Q2 and an additional $103 million already in Q3. Our strong cash flow generation, robust financial profile and continued execution of our proven strategy give us confidence in our ability to build on our success to drive growth well into the future.”

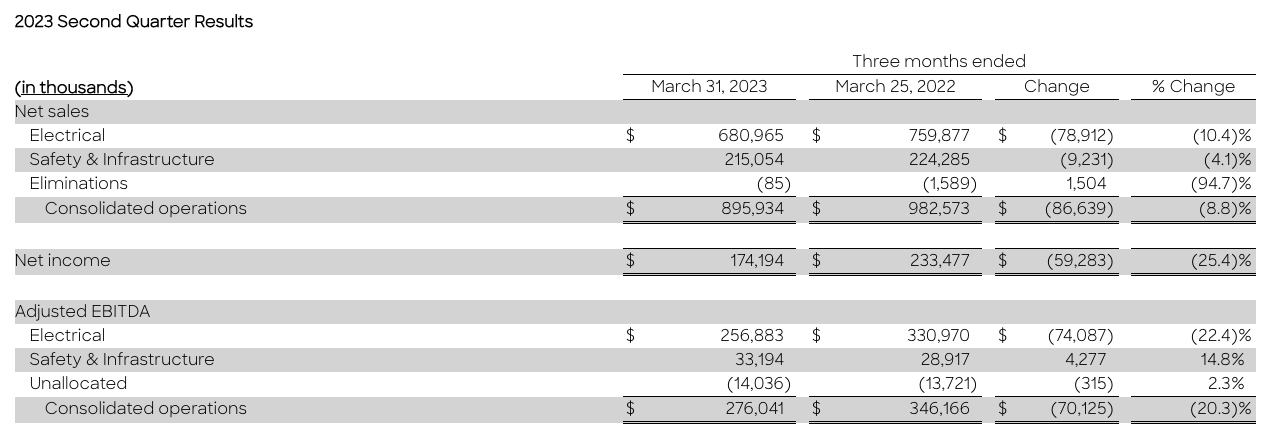

Net sales decreased by $86.6 million, or 8.8%, to $895.9 million for the three months ended March 31, 2023, compared to $982.6 million for the three months ended March 25, 2022. The decrease in net sales is primarily attributed to decreased average selling prices across the Company’s products of $168.7 million as a result of expected pricing normalization. This decrease was partially offset by increased net sales of $49.5 million from companies acquired during fiscal 2022 and fiscal 2023 and increased sales volume of $40.9 million.

Gross profit decreased by $63.5 million, or 15.3%, to $352.9 million for the three months ended March 31, 2023, as compared to $416.4 million for the prior-year period. Gross margin decreased to 39.4% for the three months ended March 31, 2023, as compared to 42.4% for the prior-year period. Gross profit decreased primarily due to declines in average selling prices of $168.7 million partially offset by slower declines in the costs of steel, copper and PVC resin of $91.8 million, and companies acquired during fiscal 2022 and 2023 of $11.7 million.

Net income decreased by $59.3 million, or 25.4%, to $174.2 million for the three months ended March 31, 2023 compared to $233.5 million for the prior-year period primarily due to lower gross profit and higher selling, general and administrative costs, intangible amortization and interest expense.

Adjusted EBITDA decreased by $70.1 million, or 20.3%, to $276.0 million for the three months ended March 31, 2023 compared to $346.2 million for the three months ended March 25, 2022. The decrease was primarily due to lower gross profit.

Net income per diluted share prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) was $4.31 for the three months ended March 31, 2023, as compared to $5.08 in the prior-year period. Adjusted net income per diluted share decreased by $0.52 to $4.87 for the three months ended March 31, 2023, as compared to $5.39 in the prior year period. The decrease in diluted earnings per share is primarily attributed to lower net income.

Segment Results

Electrical

Net sales decreased by $78.9 million, or 10.4%, to $681.0 million for the three months ended March 31, 2023 compared to $759.9 million for the three months ended March 25, 2022. The decrease in net sales is primarily attributed to decreased average selling prices of $115.0 million, decreased sales volume of $4.9 million and the unfavorable impact of foreign exchange rates of $5.4 million. These decreases were partially offset by increased net sales of $47.9 million from companies acquired during fiscal 2022 and fiscal 2023.

Adjusted EBITDA for the three months ended March 31, 2023 decreased by $74.1 million, or 22.4%, to $256.9 million from $331.0 million for the three months ended March 25, 2022. Adjusted EBITDA margins decreased to 37.7% for the three months ended March 31, 2023 compared to 43.6% for the three months ended March 25, 2022. The decrease in Adjusted EBITDA and Adjusted EBITDA margins was largely due to lower average selling prices over input costs.

Safety & Infrastructure

Net sales decreased by $9.2 million, or 4.1%, for the three months ended March 31, 2023 to $215.1 million compared to $224.3 million for the three months ended March 25, 2022. The decrease is primarily attributed to decreased average selling prices of $53.7 million driven by lower input costs of steel, partially offset by higher volumes of $45.8 million, primarily in the mechanical tube, construction and metal framing product lines, and increased net sales of $1.6 million from companies acquired during fiscal 2022.

Adjusted EBITDA increased by $4.3 million, or 14.8%, to $33.2 million for the three months ended March 31, 2023 compared to $28.9 million for the three months ended March 25, 2022. Adjusted EBITDA margins increased to 15.4% for the three months ended March 31, 2023 compared to 12.9% for the three months ended March 25, 2022. The Adjusted EBITDA increase is primarily due to increased volume.

Full-Year Outlook1

The Company is increasing its estimate for fiscal year 2023 Adjusted EBITDA and Adjusted net income per diluted share. The Company estimates Adjusted EBITDA to be approximately $1,015 million to $1,065 million, and Adjusted net income per diluted share to be in the range of $17.45 – $18.35.

The Company notes that this perspective may vary due to changes in assumptions or market conditions and other factors described under “Forward-Looking Statements.”

_______________

¹ Reconciliations of the forward-looking full-year 2023 outlook for Adjusted EBITDA and Adjusted net income per diluted share are not being provided as the Company does not currently have sufficient data to accurately estimate the variables and individual adjustments for such reconciliations. Accordingly, we are relying on the exception provided by Item 10(e)(1)(i)(B) of Regulation S-K to exclude these reconciliations.