FARGO, N.D., Oct. 20, 2025 — At Border States, keeping you informed about the state of our supply chain remains a top priority. Across the core markets we serve (construction, industrial and utility), our industry continues to see a mix of resiliency and stabilization, coupled with persistent headwinds. As always, we aim to provide timely insights to help you plan your business with confidence. While accurate to the best of our knowledge, the information in this letter reflects current conditions and may evolve rapidly.

October began with a federal government shutdown that has now extended into its third week, further stressing economic uncertainty in our country. At Border States, our customers continue to respond to rising energy demands, digitalization and labor pressures, and infrastructure modernization needs. From AI-driven data center expansion and investment in automated manufacturing to electrification, these forces are reshaping the demand and requirements of the global supply chain.

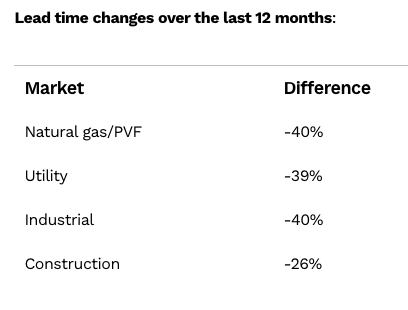

Lead Time Trends

Government shutdown poses a risk to the economy

Ocean freight rates continue to fall amid soft demand

Ocean shipping rates have fallen across major freight lanes due to tariffs, overcapacity and soft demand.

By the numbers: September import volumes dropped 8% from August and 8% year-over-year, with imports from China down 12% month-over-month and 23% last year as importers shift volumes to other countries.

The big picture: Carriers are canceling sailings to stabilize rates, reducing service reliability. Meanwhile, the first phase of a peace deal between Israel and Hamas raises hopes for recovery in the Suez Canal. Still, security risks from Houthi rebel attacks continue to pose threats to Red Sea shipping, experts say, and recovery won’t happen immediately.

New tariffs and rules reshape the trucking market

The U.S. trucking industry continues to struggle with weak demand and historically low spot rates, generally favoring shippers.

Why it matters: Incoming tariffs on heavy-duty truck imports and new rules, including the Federal Motor Carrier Safety Administration restricting non-domiciled Commercial Driver’s Licenses, are reshaping the market. Many shippers have front-loaded imports to avoid tariff impacts, which is impacting Q4 volumes.

The big picture: While flatbed segments are showing some capacity tightening, the overall market recovery remains uncertain. New truck orders are down 20% year over year, signaling caution among carriers. Market softness is expected to persist into early 2026 with no clear path to recovery.

Ceasefire plan eases commodity market pressure

Commodity markets, from copper to crude oil, are under pressure from various factors, including geopolitical tensions, supply chain disruptions and trade policy changes. A breakthrough in the Middle East eased some uncertainty, when Israel and Hamas agreed to the first phase of a ceasefire plan.

By the numbers: Copper prices are expected to rise more than 12% in the next two years due to supply constraints and robust demand from clean energy and AI sectors. The domestic aluminum and steel industries are affected by trade policies and demand shifts, including a 4.4% drop in aluminum demand in the United States and Canada, and a 16.8% drop in U.S. steel imports. Lumber futures fell to nearly $525 per thousand board feet. Brent Crude futures fell 0.8% while West Texas Intermediate fell 0.7% on October 15.

The bottom line: Commodity markets remain in flux as supply disruptions, trade policies and shifting demand continue to drive short-term price swings.

Tagged with Biggest News, Border States, supply chain