ST. LOUIS — Emerson today reported results for the first fiscal quarter ended December 31, 2020.

ST. LOUIS — Emerson today reported results for the first fiscal quarter ended December 31, 2020.

First quarter GAAP net sales were flat and underlying sales were only down 2 percent excluding favorable currency of 1 percent and impact from acquisitions of 1 percent. Revenue for the quarter was ahead of management’s November guidance, with both business platforms finishing above expectations. Overall, the company continued to see a sharp bifurcation in North American markets, with residential markets showing continued strength while many core automation markets remained subdued. Overall, North America was down high single-digits in the quarter. All other regions trended to growth with Europe up mid single-digits and Asia, Middle East & Africa up low single-digits.

December trailing three-month underlying orders were only down 4.5 percent, ahead of previous expectations, as strength in residential-facing, cold chain, life sciences, medical, and food & beverage markets was more than offset by ongoing weakness in many process industries. Commercial & Residential Solutions trailing three-month underlying orders showed continued strength, up 15 percent, with growth across all businesses and geographies. Additionally, Automation Solutions trailing three-month underlying orders continued to stabilize, down 13 percent, as KOB3 demand was steady and KOB2 demand improved slightly.

First quarter gross profit margin of 41.4 percent was down 100 basis points from the previous year primarily due to deleverage and business mix. Pretax margin of 13.5 percent and EBIT margin of 14.5 percent were up 330 basis points and 350 basis points, respectively, as ongoing comprehensive cost reduction actions took effect. Adjusted EBIT margin, which excludes restructuring and first year purchase accounting charges and fees, was 16.3 percent for the quarter, up 260 basis points.

GAAP earnings per share was $0.74 for the quarter, up 40%, and adjusted earnings per share was $0.83, up 24 percent. Earnings in the quarter exceeded management guidance and benefited significantly from better volume, as well as ongoing restructuring and cost reduction actions.

Operating cash flow was $808 million for the quarter, up 90 percent. Free cash flow was $686 million, up 121 percent for the quarter, resulting in strong free cash flow conversion of 152 percent. Cash flow results reflected higher earnings due to rigorous operational execution across the two business platforms and favorable trade working capital management.

“Emerson’s leadership team and global operations remain steadfastly focused on safely serving customers and protecting business continuity in essential industries including life sciences, power, food and beverage, home comfort, energy, and water,” said Emerson Chairman and CEO David N. Farr. “Our dedicated team across the globe continues to make me proud as they work tirelessly to help our customers navigate ongoing industry and macroeconomic turbulence. As more COVID-19 vaccines are approved and begin to be distributed, we remain optimistic for some stabilization in the second half of the year. In the meantime, we will continue to operate nimbly and safely to serve our customers in vital industries.

“Orders and sales continued their upward trajectory in the quarter, and operating results exceeded expectations. These factors enabled us to deliver strong profitability, earnings and cash flow, driven by our ongoing robust cost containment and restructuring actions, as well as improvement in some of our end markets. As the broader macroeconomic outlook continues to stabilize, we are well-positioned with a more agile, lean, and technology-centric organization going forward.”

Business Platform Results

Automation Solutions net sales decreased 6 percent in the quarter, with underlying sales down 9 percent, which was ahead of November guidance. The improvement in orders and sales was primarily driven by European power, chemical, and life sciences markets, and energy markets in Asia, Middle East & Africa.

In the Americas, underlying sales were down 20 percent, resulting from continued broad-based demand challenges, particularly in North America. These challenges were partially offset by continued momentum in life sciences, food & beverage, and semiconductor markets, as well as some early signs of improvement in upstream energy markets. Europe underlying sales were up 2 percent, driven by strength in Eastern Europe. Asia, Middle East & Africa underlying sales remained positive in the low single-digits, as strength in China (up 6 percent) and the rest of Asia (up 7 percent) was offset by weakness in the Middle East & Africa.

December trailing three-month underlying orders were down 13 percent, consistent with November and reflecting ongoing weakness, but stabilization, across many key automation end markets. However, growth momentum continues in life sciences, medical, food & beverage, and semiconductor markets. Geographically, the Americas continue to be most challenged, down 27 percent. Asia, Middle East & Africa declined modestly by 1 percent, supported by China orders growing 6 percent. Europe declined by 3 percent due to weakness in energy markets somewhat offset by chemical, power and life science projects. Backlog in the business finished the quarter at $5.3 billion, an increase of approximately $600 million (of which the OSI acquisition represented approximately $300 million). Lastly, OSI had a strong first quarter as a part of the Emerson team, booking nearly $100 million of orders, reflecting early momentum well above revenue synergy plans. Overall, while the global demand environment stabilizes and begins to improve, key North American markets remain challenged for the Automation Solutions business, but they have stabilized and appear to be turning.

Segment EBIT margin increased 250 basis points to 13.4 percent, on down sales, as savings from cost actions and favorable price-cost more than offset volume deleverage and mix. Adjusted segment EBIT margin, which excludes restructuring and related costs, increased 200 basis points to 15.8 percent. Total restructuring and related actions in the quarter totaled $64 million.

Commercial & Residential Solutions net sales increased 13 percent in the quarter, with underlying sales up 12 percent. Underlying sales in the Americas were up 14 percent, reflecting strong demand in residential markets and improvement in the cold chain business. Similarly, Europe was up 8 percent as heat pump demand was driven by sustainability regulations and customer technology preferences. Asia, Middle East & Africa was up 7 percent, with China leading, up 10 percent.

December trailing three-month underlying orders were up 15 percent, reflecting growth across all businesses and geographies. Continued strength in residential markets and positive momentum in cold chain markets were key drivers. Geographically, North America increased by 16 percent as residential HVAC and home products markets continued to show robust demand. Additionally, cold chain markets improved with vaccine distribution infrastructure and food safety investment. Asia, Middle East & Africa orders increased by 17 percent, highlighted by growth in China of 17 percent. Europe grew by 10 percent, as demand for heat pump and efficient appliance solutions continued its momentum due to sustainability regulations and customer technology preferences. Lastly, backlog increased by approximately $200 million to end the quarter at nearly $800 million.

Segment EBIT margin increased 280 basis points to 21.0 percent driven by strong leverage combined with previous cost reduction actions. Adjusted segment EBIT margin, which excludes restructuring and related costs, increased 230 basis points to 21.2 percent. Total restructuring and related actions in the quarter were $3 million.

2021 Updated Outlook

As macroeconomic uncertainties related to COVID-19 begin to slowly wane, we continue to expect a slow-but-steady improvement in industrial demand over the course of 2021 as more vaccines become available and distribution methods mature. We also expect that residential demand for many of our markets around the world will remain robust through the year.

Within this framework, we now expect underlying revenue to be positive for the full year. However, due to the delayed recovery timeline in many key automation markets, especially in North America, we remain committed to our plan of total company restructuring spend of approximately $200 million for the full year. Lastly, the updated guidance assumes no major operational or supply chain disruptions and oil prices in the $45 to $55 range for the remainder of the year.

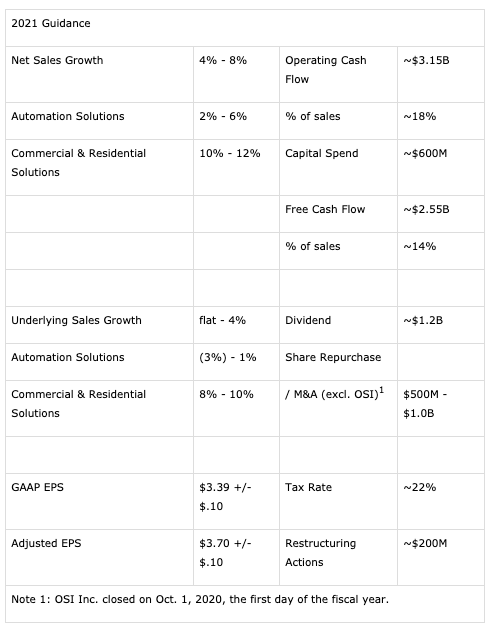

The following table summarizes the updated 2021 guidance framework:

“Looking ahead to the remainder of the fiscal year, we will continue to invest in core technologies, software solutions, and other capabilities that strengthen our position in attractive and growing marketplaces, including alternative fuels, renewable energy, power transmission and distribution, and life sciences, among others,” Farr said. “Digital transformation and ESG initiatives continue to gain momentum among many of our industrial customers, and these portfolio enhancements and development efforts will enable us to help more customers not only adapt, but truly excel in their new operating realities post-pandemic.”

Tagged with Emerson, financial results