![]() ST. LOUIS, May 5, 2021 – Emerson today reported results for the second fiscal quarter ended March 31, 2021.

ST. LOUIS, May 5, 2021 – Emerson today reported results for the second fiscal quarter ended March 31, 2021.

“I remain proud, humbled, and energized by the exceptional advances and adaptability I’m seeing across the enterprise,” said Emerson President and CEO Lal Karsanbhai. “We have two major concurrent themes building momentum within the organization. First, the enthusiasm and progress around modernizing our culture is palpable, particularly with regard to diversity and inclusion, work practices, and talent management. These initiatives are not just good practice, but are expected to be key business enablers for Emerson’s outperformance and value creation going forward. We will share more details on this vital work and our overall sustainability progress in our upcoming ESG Report which will be published in June.

“Secondly, economic recovery momentum is building across most of our key end markets, which resulted in better than expected top line results this quarter. Trailing three month underlying orders ended on the high side of the guided range, and underlying sales came in above guidance – a strong signal for broadening recovery. Residential markets and shorter cycle automation markets continue to show strength, while commercial and longer cycle automation markets should continue their steady recovery during the second half of the year. Importantly, we will continue to drive the remaining elements of our comprehensive cost reset plan as we target achieving record margins. Lastly, we are accelerating investment in innovation and key technologies that drive differentiation, create value for our customers, and are aligned with global macrotrends such as sustainability and digital transformation.”

Second quarter Net Sales were up 6 percent and Underlying Sales were up 2 percent, excluding favorable currency of 3 percent and an impact from acquisitions of 1 percent. Revenue for the quarter was ahead of management’s February guidance, with both business platforms finishing above expectations. The Americas improved sequentially, but was down 4 percent year over year, as residential and cold chain strength was more than offset by a more sluggish process automation recovery. Europe was up 7 percent, while Asia, Middle East & Africa grew by 12 percent, driven by China which recovered sharply by 45 percent.

March Trailing Three-Month Underlying Orders were up 4 percent (improved from down 2 percent in February), in the upper portion of guidance, as strength in residential, cold chain, professional tools, hybrid and discrete automation markets more than offset later cycle process automation markets.

Second quarter Gross Profit Margin of 42.0 percent was down 10 basis points from the previous year primarily due to business mix, as the recovery in Commercial & Residential Solutions outpaced Automation Solutions. Pretax Margin of 16.6 percent was flat while EBIT Margin of 17.5 percent was up 10 basis points, as ongoing comprehensive cost reduction actions were largely offset by higher costs due to the mark-to-market stock compensation plan, which produced an unfavorable impact of 230 basis points. The stock price in the prior year was sharply lower than current year as a result of the pandemic induced drop. Adjusted EBIT Margin, which excludes restructuring and first year purchase accounting charges, was 18.2 percent for the quarter, down 20 basis points.

Earnings Per Share were $0.93 for the quarter, up 11 percent, and Adjusted Earnings Per Share were $0.97, up 9 percent. Earnings in the quarter exceeded management guidance, benefiting from better volume and ongoing cost reduction actions.

Operating Cash Flow was $807 million for the quarter, up 37 percent, and $1.6 billion year-to-date, up 60 percent. Free Cash Flow was $707 million, up 48 percent for the quarter, resulting in strong free cash flow conversion of 125 percent. Year-to-date, Free Cash Flow was $1.4 billion, up 77 percent. Cash flow results reflected higher earnings due to operational execution across the two business platforms and favorable trade working capital.

Business Platform Results

Automation Solutions net sales increased 3 percent in the quarter, with underlying sales down 2 percent, which was ahead of February guidance. Results reflected ongoing strength across discrete and hybrid markets, and improvement across MRO and installed base programs (KOB3). Discrete oriented businesses grew high single digits, while systems and software grew low single digits. Recovery in the Americas continues to lag, but exceeded our expectations and showed sequential improvement with underlying sales down 12 percent compared to down 20 percent in Q1. Continued momentum in life sciences, food & beverage, and medical markets paired with lagging but stabilizing trends across most process industries. Europe underlying sales were up 6 percent, driven by power and biofuels demand. Asia, Middle East & Africa underlying sales grew 9 percent, as recovery in China (up 42 percent), more than offset softness in SE Asia and the Middle East.

March trailing three-month underlying orders were down 5 percent (improvement from down 9 percent in February), reflecting an ongoing lagging recovery in many process automation markets, partially offset by strength across most discrete and hybrid automation markets. Importantly, however, process automation MRO and installed base targeted programs (KOB3) showed sequential improvement. The Americas improved, but continues to be the trailing geography, down 10 percent. Asia, Middle East & Africa declined modestly by 4 percent, supported by China orders increasing sharply by 19 percent, largely driven by demand in discrete markets. Europe was up by 7 percent, also supported by discrete businesses. Backlog was unchanged from the prior quarter at $5.3 billion, but was up 14 percent year-to-date.

Segment EBIT margin increased 240 basis points to 16.8 percent, on down sales, as savings from cost actions and favorable price-cost more than offset volume deleverage and mix. Adjusted segment EBIT margin, which excludes restructuring and related costs, increased 180 basis points to 17.3 percent. Total restructuring and related actions in the quarter totaled $14 million.

Commercial & Residential Solutions net sales increased 13 percent in the quarter, with underlying sales up 11 percent, at the top end of previous guidance. Underlying sales in the Americas were up 8 percent, reflecting continued strong demand in residential markets and improvement in cold chain and professional tools businesses. Similarly, Europe was up 9 percent as heat pump demand was driven by sustainability regulations and customer technology preferences. Asia, Middle East & Africa was up 24 percent, bolstered by China, up 56 percent due to strong commercial HVAC and cold chain demand.

March trailing three-month underlying orders were up 21 percent (improvement from up 14 percent in February), with high single digit or double digit growth across all businesses and geographies. Ongoing strength in residential facing markets was bolstered by cold chain and professional tools momentum. The Americas was up 19 percent, while Europe was up 15 percent, driven by demand for heat pumps and other energy efficient appliance technologies. Asia, Middle East & Africa orders increased by 32 percent, driven by growth in China of over 60 percent. Backlog increased by approximately $200 million in the quarter, ending at a record $1.0 billion. Backlog was up 58 percent year-to-date.

Segment EBIT margin increased 70 basis points to 21.7 percent as leverage and cost reductions were somewhat offset by price-cost headwinds. Adjusted segment EBIT margin, which excludes restructuring and related costs, increased 40 basis points to 22.0 percent. Total restructuring and related actions in the quarter totaled $5 million

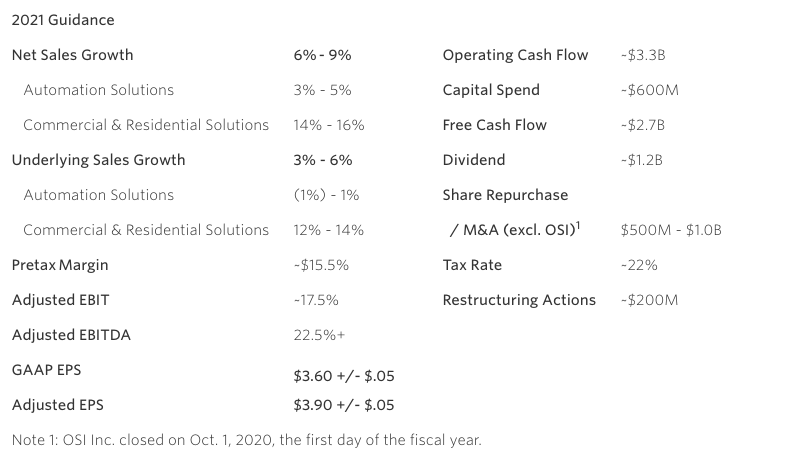

2021 Updated Outlook

Despite ongoing pandemic challenges in some parts of the world, we expect overall continued improvement in industrial and commercial demand over the remainder of 2021. We also expect that residential demand will remain robust, but begin to taper in the second half.

The following table summarizes the updated 2021 guidance framework: