HIGHLAND HEIGHTS, Ky. — General Cable Corporation (NYSE: BGC) reported results for the fourth quarter ended December 31, 2014. For the fourth quarter of 2014, the Company recorded adjusted earnings per share of $0.15 and adjusted operating income of $46 million, in line with management’s guidance. For the fourth quarter of 2014, reported loss per share was $2.86 and reported operating income was $14 million. For the full year 2014, the Company generated adjusted operating cash flow of $212 million and reported operating cash flow of $134 million.

Gregory B. Kenny, President and Chief Executive Officer, said, “We are making significant progress on our divestiture and restructuring programs and will remain focused on the execution of these strategic initiatives to simplify our geographic portfolio, reduce complexity and lower the cost base of our core operations. The sale of our interest in the Philippines marked a very important first step in executing on our divestiture program. With the fourth quarter announcement of restructuring actions to be taken in North America and Latin America, which are anticipated to generate approximately $15 million or 20% of the total annual savings of $75 million, we have now announced substantially all planned initiatives as outlined in July 2014. We are continuing to carefully evaluate further restructuring actions in our core operations as we focus on delivering increased returns from our businesses in North America, Latin America and Europe in an ongoing difficult operating environment most recently characterized by the impact of volatile metal prices and lower oil prices. The search for the next CEO and an operations-experienced independent director is progressing under the guidance of our outside Directors.”

Brian J. Robinson, Executive Vice President and Chief Financial Officer, said, “We generated $212 million of adjusted operating cash flow for 2014 principally due to the strong management of working capital particularly inventory during the fourth quarter. We applied the proceeds from the sale of the Philippines toward the reduction of debt, a key priority for the Company. Our liquidity position is strong as availability under our North American and European based credit facility increased to $425 million. We also maintain an incremental $120 million of liquidity throughout Latin America (excluding Venezuela) including cash and various local working capital lines. We are well positioned to fund the business including working capital requirements, restructuring activities, quarterly dividends and the retirement of our $125 millionsenior floating rate notes due in April 2015.”

Q4 2014 versus Q4 2013

Net sales for the fourth quarter of 2014 of $1,547 million were down 6% as compared to the fourth quarter of 2013 on a metal adjusted basis. Unit volume in the Company’s core operations consisting of North America, Latin America (excludingVenezuela) and Europe was down 6% year over year principally due to lower aerial transmission cable shipments in North America and Brazil as well as weaker end market demand throughout Europe. Excluding aerial transmission cables in North America and Brazil, unit volume in the Company’s core operations increased 2% year over year principally due to demand for electric utility distribution and specialty products in North America. Adjusted operating income for the fourth quarter of 2014 of $46 million was down $5 million from the fourth quarter of 2013 (excludingVenezuela from both periods). Overall, adjusted operating income for the fourth quarter of 2014 reflects the benefit of restructuring initiatives and stronger results year over year in North America which were offset by the impact of weaker demand throughout Europe.

Q4 2014 versus Q3 2014

Net sales for the fourth quarter of 2014 increased 3% as compared to the third quarter of 2014 on a metal adjusted basis. Excluding aerial transmission cables inNorth America and Brazil, unit volume for the fourth quarter of 2014 in the Company’s core operations was flat as compared to the third quarter. Sequentially, adjusted operating income was down $9 million in the fourth quarter principally due to seasonal demand trends including planned factory shutdowns.

Other expense

Effective December 31, 2014, the Company adopted the SICAD II currency exchange rate of 50 bolivars per US dollar to remeasure its local balance sheet in Venezuelawhich resulted in a reported loss of $91 million in the fourth quarter. Excluding the impact of Venezuela, other expense was $8 million for the fourth quarter which primarily reflects mark to market losses of $3 million on derivative instruments accounted for as economic hedges (principally used to manage currency and commodity risk on the Company’s global project business), and foreign currency transaction losses of $5 million.

Liquidity – Excluding Venezuela

Net debt was $1,162 million at the end of the fourth quarter of 2014, a decrease of $197 million from the end of the third quarter of 2014. The decrease in net debt is principally due to reductions in working capital and the use of cash proceeds generated from the sale of the Company’s interest in the Philippines toward the reduction of debt. The decrease in working capital principally reflects the impact of normal seasonal trends including the achievement of aggressive inventory reduction targets and the collection of submarine turnkey project milestone payments.

First Quarter 2015 Outlook for the Company’s core operations consisting of North America, Latin America and Europe (excluding Venezuela, Asia-Pacific and Africa)

Revenues in the first quarter are expected to be in the range of $1.1 to $1.15 billion. Unit volume in the Company’s core operations is anticipated to be down mid-single digits sequentially principally due to seasonal demand trends. The Company anticipates adjusted operating income to be in the range of $10 to $25 million for the first quarter. Adjusted earnings per share are expected to be in the range of $(0.16)to $(0.01) per share for the first quarter. The Company’s first quarter outlook assumes copper (COMEX) and aluminum (LME) prices of $2.60 and $0.84, respectively. The first quarter outlook does not include operating results fromVenezuela nor does it include operating results from Asia Pacific and Africa. As noted in the Segment Information, the Company has recast its segments to align with its current strategy of portfolio simplification and new management structure, including presenting a new Asia Pacific and Africa reportable segment. For accounting purposes, these operations do not meet the requirement to be presented as discontinued operations.

“Overall, we anticipate a sluggish start to the year driven by the impact of typical seasonal demand trends and much lower metal prices. The first quarter is typically our slowest period of the year due to lower construction activity principally due to seasonal weather and extended holidays. The recent decline in copper and aluminum prices is expected to be a headwind to operating results in the first quarter in the range of $15 to $20 million as we sell higher weighted average cost inventory into a lower metal cost environment under our weighted average cost accounting methodology. However, if this lower metal price environment persists, we would expect to generate cash as our investment in working capital declines. While we clearly cannot control macro economic factors, I am very pleased with our progress on what we can control including our divestiture program and further cost reduction opportunities,” Kenny concluded.

Non-GAAP Financial Measures

Adjusted operating income (defined as operating income before extraordinary, nonrecurring or unusual charges and other certain items), adjusted earnings per share (defined as diluted earnings per share before extraordinary, nonrecurring or unusual charges and other certain items), adjusted operating cash flow (defined as operating cash flows before extraordinary, nonrecurring or unusual charges and other certain items) and net debt (defined as long-term debt plus current portion of long-term debt less cash and cash equivalents) are “non-GAAP financial measures” as defined under the rules of the Securities and Exchange Commission.

These Company-defined non-GAAP financial measures are being provided herein because management believes they are useful in analyzing the operating performance of the business and are consistent with how management reviews the underlying business trends. Use of these non-GAAP measures may be inconsistent with similar measures presented by other companies and should only be used in conjunction with the Company’s results reported according to GAAP. Adjusted results and guidance reflect the removal of the impact of our Venezuelan operations on a standalone basis due to the ongoing economic and political uncertainty in that country, principally driven by the foreign currency exchange system, government-imposed profit caps/limitations and limited access to U.S. dollars for the import of raw materials. However, we expect ongoing operations in Venezuela to continue, and we cannot predict the amounts of any future income or expenses we may incur relating to our Venezuelan operations. Certain historical results of our Venezuelan operations on a standalone basis are provided in the Fourth Quarter 2014 Investor Presentation available on the Company’s website. The first quarter 2015 guidance reflects the removal of Asia Pacific and Africa operating results as we are in the process of divesting these operations and therefore cannot predict the amounts of any future operating income or expenses we may incur.

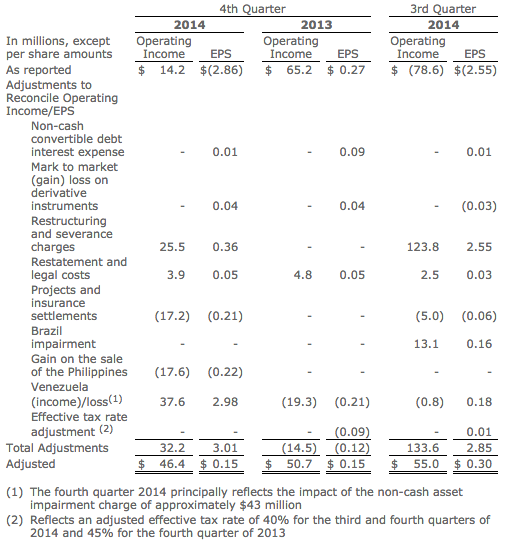

A reconciliation of adjusted operating income to reported operating income and adjusted earnings per share to reported earnings per share for the fourth quarter of 2014 and 2013 and the third quarter of 2014 is set forth in the table below. A reconciliation of adjusted operating cash flows to reported operating cash flow is included in the Company’s Fourth Quarter 2014 Investor Presentation available on the Company’s website. With respect to the Company’s expected first quarter 2015 adjusted operating income and adjusted earnings per share, the Company is not able to provide a reconciliation of these non-GAAP financial measures to GAAP because it does not provide specific guidance for the various extraordinary, nonrecurring or unusual charges and other certain items. These items have not yet occurred, are out of the Company’s control and/or cannot be reasonably predicted. As a result, reconciliation of the non-GAAP guidance measures to GAAP is not available without unreasonable effort and the Company is unable to address the probable significance of the unavailable information.

A reconciliation of operating income and earnings per share to adjusted non-GAAP operating income and earnings per share follows:

(To view the entire report with tables, click here.)

Tagged with General Cable, tED