NEW YORK (BUSINESS WIRE) — New construction starts in October climbed 21% to a seasonally adjusted annual rate of $864.0 billion, according to Dodge Data & Analytics. The substantial increase followed three straight months of decline, during which the pace of total construction starts fell 22% from the exceptionally strong volume reported back in June. Nonresidential building in October surged 53%, as several very large projects lifted the manufacturing plant, office building, and transportation terminal categories. Nonbuilding construction in October advanced 14%, supported by growth for public works while the electric utility/gas plant category bounced back from depressed activity in September. Residential building in October edged up a slight 2%, helped by improvement for multifamily housing. During the first ten months of 2018, total construction starts on an unadjusted basis were $679.1 billion, up 1% from the same period a year ago. The year-to-date gain for total construction starts was restrained by a 45% slide for the electric utility/gas plant category. If the electric utility/gas plant category is excluded, total construction starts during the first ten months of 2018 would be up 3% relative to the same period a year ago.

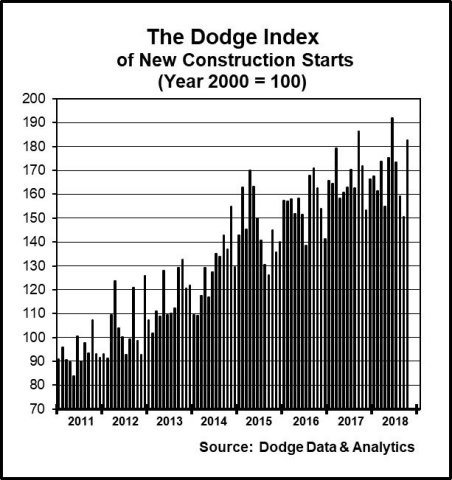

October’s data raised the Dodge Index to 183 (2000=100), up from September’s 150, marking the second highest reading for the Dodge Index so far in 2018 after June’s 192. Through the first ten months of 2018, the Dodge Index averaged 169, up slightly from the full year 2017 average of 166.

“During 2018, the presence of very large projects in a given month has played a considerable role in shaping the monthly pattern of activity, and in October it was nonresidential building that especially benefitted from the start of very large projects,” stated Robert A. Murray, chief economist for Dodge Data & Analytics. “These included a $2.4 billion petrochemical plant in Texas, the $1.4 billion Terminal One building at Newark Liberty International Airport, the $860 million expansion to the Las Vegas Convention Center, a $750 million Facebook data center in Utah, and a $655 million concourse expansion at Denver International Airport that’s part of that facility’s extensive upgrade. Earlier, decreasing construction starts for nonresidential building during this year’s third quarter raised some concern, suggesting that this sector may have already peaked and is now in decline. The strong October performance indicates that nonresidential building construction starts continue to proceed at an elevated pace, at least for the present.”

Murray continued, “The current year has also witnessed moderate growth for public works construction, helped by the greater federal funding for fiscal 2018 passed by Congress back in March as part of the omnibus appropriations legislation. For fiscal 2019 which began on October 1, the federal-aid highway program and EPA construction-related programs are operating under a continuing resolution through December 7, waiting for Congress to finalize spending levels. As for residential building, multifamily housing has shown renewed expansion this year after settling back in 2017, yet a more cautious lending stance by banks towards multifamily development may dampen multifamily construction starts next year.”

Nonresidential building in October was $358.3 billion (annual rate), up 53% from September’s lackluster amount. After registering heightened activity in June, nonresidential building retreated for three consecutive months before October’s upturn. Manufacturing plant construction in October jumped 189%. The commercial building structure types as a group increased 48% in October, strengthening after declines during the previous three months. New office construction starts in October climbed 123%. Hotel construction in October advanced 59%. Warehouse construction in October grew 17%. There were two commercial structure types that registered declines in October – commercial garages, down 5%; and store construction, down 16%.

The institutional side of nonresidential building increased 28% in October. Transportation terminal construction starts jumped 92%. The amusement and recreational category in October climbed 89%. The healthcare facilities category had a strong October. Also showing growth in October was the public buildings category, up 95% from a weak September. Educational facilities, the largest institutional category, ran counter to most of the other institutional structure types with an 18% decline in October. The religious building category also weakened in October, dropping 18%.

Nonbuilding construction in October was $184.0 billion (annual rate), up 14% following September’s 13% decline. The electric utility/gas plant category increased 187% relative to a very weak September, although October’s volume was still 32% less than the average monthly pace reported during 2017. The public works categories as a group rose 6% in October, with a varied performance by individual category. Highway and bridge construction starts climbed 26%, with October coming in as the highest seasonally adjusted monthly amount so far in 2018. The top five states ranked by the dollar amount of highway and bridge construction starts in October were – Texas, Michigan, Florida, California, and Pennsylvania. River/harbor development in October advanced 114%. Water supply construction grew 30% in October. The miscellaneous public works category pulled back 33% in October from its heightened September pace. Through the first ten months of 2018, pipeline construction starts totaled $19.3 billion, down only 8% from the robust amount during the same period of 2017. Sewer construction also retreated in October, falling 40%.

Residential building in October was $321.7 billion (annual rate), rising 2%. The lift came from multifamily housing, which increased 15% in October. Through the first ten months of 2018, the top five metropolitan areas ranked by the dollar amount of multifamily starts (with their percent change from a year ago) were – New York NY (up 3%), Boston MA (up 91%), Miami FL (up 44%), Washington DC (up 20%), and Seattle WA (up 25%). Metropolitan areas ranked 6 through 10 were – San Francisco CA (up 11%), Los Angeles CA (down 31%), Dallas-Ft. Worth TX (up 24%), Atlanta GA (down 15%), and Chicago IL (down 43%). Single-family housing in October decreased 4%, as affordability constraints continue to make it difficult for this project type to register any sustained upward movement during 2018. By geography, October showed single-family declines in four of the five major regions – the Northeast, down 10%; the South Central, down 8%; the West, down 6%; and the Midwest, down 5%. Only the South Atlantic, growing 4%, was able to post a single family gain in October.

The 1% increase for total construction starts on an unadjusted basis during the first ten months of 2018 was due to mixed behavior by the three major construction sectors. Residential building maintained its 6% lead over last year, with the dollar amount for both single-family housing and multifamily housing up 6%. Nonresidential building year-to-date slipped 2%, with institutional building down 8%, commercial building down 3%, and manufacturing building up 32%. Nonbuilding construction year-to-date dropped 4%, as a 5% increase for public works was outweighed by the 45% plunge for electric utilities/gas plants. By major region, total construction starts during the January-October period of 2018 showed this pattern compared to a year ago – the South Central, up 11%; the Midwest and South Atlantic, each up 5%; the West, down 1%; and the Northeast, down 18%. The year-to-date decline in the Northeast was relative to the robust first ten months of 2017.

Copyright 2018 The Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

Tagged with AP, construction, economy