Copper is on a downward streak as the red metal lost ground on the London Metal Exchange (LME) for the fourth straight session. Copper prices have fallen nearly 6% so far this year in anticipation of an economic slowdown in China. Analysts point to the red metal’s recent slide as more of a cautionary approach heading into the start of the Federal Reserve’s two-day meeting today. Another key factor in copper’s recent run of bad luck is a slightly stronger dollar.

Frequent tED contributor Andrew Hecht is always looking at the big picture when it comes to copper and commodities. He points to the longer history of the dollar, not just the recent surge. “Since January 2017, the move to the downside in the U.S. dollar has been another supportive factor for the price of copper,” states Hecht. “If the dollar continues to decline in value and economic growth increases over the months ahead, we are likely to see more demand for copper leading to another higher high. The last time copper traded above the $4 per pound level was back in 2011, and there are lots of levels of technical resistance on the way back to that lofty level.”

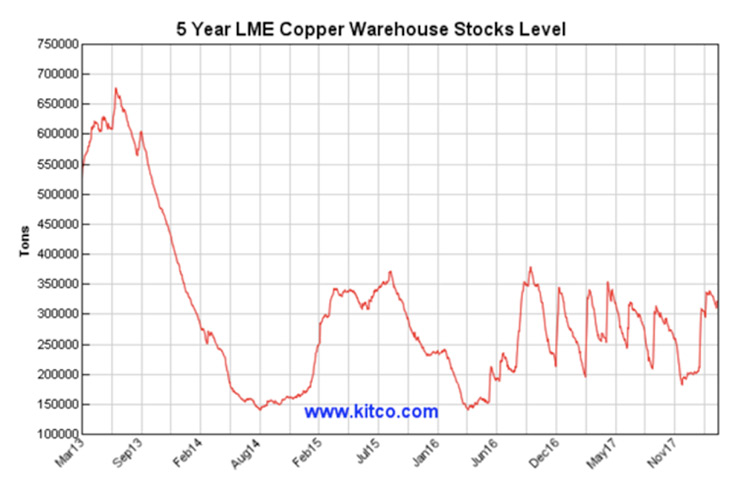

That is a long way from the current level of $3.06/pound at the time of this writing. Click on the chart above to get current pricing. The aforementioned LME inventory is also a key factor to Hecht’s outlook to a possible ascent to $4. While three-month copper on the LME has fallen to $6,836, it’s the amount of copper inventory that is key. As the chart below shows, inventories on the LME have fallen drastically since 2013.

Source: LME

“Copper is hanging in there above support and the metal reflects the health of the global economy,” Hecht adds. “These days many signs are telling us that the prospect for more price appreciation in copper in the month ahead is strong and building a long position on weakness could be the optimal way to approach the red metal when it comes to both trading and investing.”

The Week Ahead

The G20 meeting in Argentina is underway and the threat of trade wars will be in focus this week. The highlight (if you want to call it that) of the upcoming week is the Fed wrapping up its two-day policy meeting tomorrow. All bets are on the Fed raising rates by a quarter point tomorrow.

Here is a complete list of significant events likely to affect the markets this week, thanks to investing.com.

Tuesday, March 20

The Reserve Bank of Australia is to publish the minutes of its latest policy setting meeting. Australia is also to publish data on house price inflation.

The UK is to publish data on inflation.

The ZEW Institute is to report on German economic sentiment.

The G20 summit in Buenos Aires is to continue for a second day.

Wednesday, March 21

Financial markets in Japan will be closed for a holiday.

The UK is to publish its latest employment report.

The U.S. is to report on existing home sales.

The Federal Reserve is to announce its latest monetary policy decision and publish its rate statement, which outlines economic conditions and the factors affecting the decision.

Thursday, March 22

The Reserve Bank of New Zealand is to announce its latest monetary policy decision.

Australia is to publish its latest employment report.

The euro zone is to release data on manufacturing and service sector activity.

The UK is to release data on retail sales. Later in the day, the Bank of England is to announce its rate decision.

The U.S. is to publish the weekly report on jobless claims.

Friday, March 23

Canada is to publish data on retail sales and inflation.

The U.S. is to round out the week with reports on durable goods orders and new home sales.